10 / 236

10 / 236

RISK FACTORS

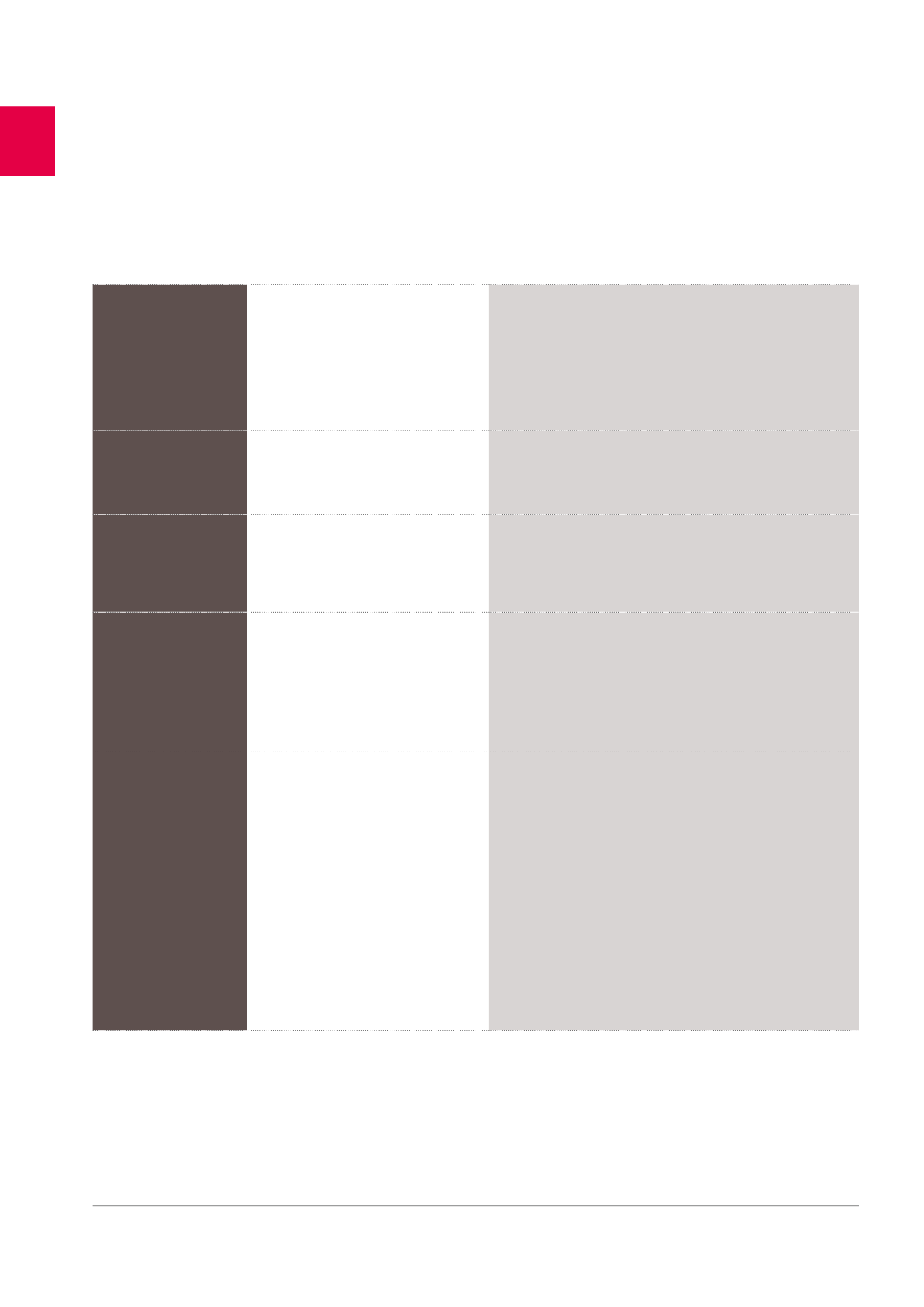

DESCRIPTION OF THE RISK POTENTIAL IMPACT

MITIGATING FACTORS AND MEASURES

Non-compliance with RREC

regime

1. Loss of approval as RREC and the

associated fiscal transparency regime

(exemption from income tax at RREC level/

taxation at shareholder level).

2. Compulsory early repayment of certain

loans.

Professionalism of the teams ensuring rigorous compliance with the

obligations.

Non-compliance with SIIC

or FBI regime

Loss of the fiscal transparency regime.

Professionalism of the teams ensuring rigorous compliance with

obligations.

Unfavourable changes

to the RREC, SIIC or FBI

regimes

Fall in the results or the net asset value.

Regular contact with public authorities. Participation in organisations and

federations representing the sector.

Changes to town-

planning or environmental

legislation

1. Reduction in the fair value of the property.

2. Increase in the costs to be incurred to be

able to operate a property.

3. Unfavourable effect on the capacity of the

Group to operate a property.

Active energy performance and environmental policy for the offices,

anticipating the legislation as far as possible.

Changes to the social

security system for

healthcare real estate:

reduction in social

security subsidies to the

operators not offset by

an increase in the prices

paid by residents or by

the intervention of private

insurers. In Belgium, since

01.07.2014, transfer of

responsibilities in terms

of healthcare and care

of elderly people from

the Federal level to the

Communities’ level.

Impact on the solvency of healthcare real

estate operators.

Annual solvency analysis of the operators on the basis of regular financial

reporting.

Monitoring of the regulatory trends.

LEGISLATION

Cofinimmo benefits from a favourable tax regime (RREC in Belgium, SIIC

in France, FBI in the Netherlands) which exempts it from corporate tax

in return for an obligation to distribute 80%

1

(Belgium), 95% (France)

2

or

100% (Netherlands) of its profits (see pages 219 and 221).

Apart from the obligations relating to company law, the company is

also required to comply with the legislation on listed companies. It is

also subject to the specific town-planning and environmental protec-

tion legislation.

1

RRECs communicate a dividend policy corresponding to an amount per share. This amount per share can be higher than or equal to 80% of the net income as required by the Royal

Decree of 13.07.2014.

2

Obligation to distribute 95% of its profits arising from the letting of property assets as from 2014.

6